Yes, most car dealerships accept personal checks without hesitation for the full purchase and downpayment of the cars. You may come across dealerships that hesitate, but that number is minimal.

Acceptance is more likely if the check is from an in-state client, drawn on an in-state bank, and not a low check number or counter-check. However, dealers may verify the check through scanning, calling the bank, or using verification systems.

There might be a hold for new cars until the check clears, and some extenuating circumstances may affect the decision. Dealerships often prefer financing arrangements to avoid high credit or debit card fees.

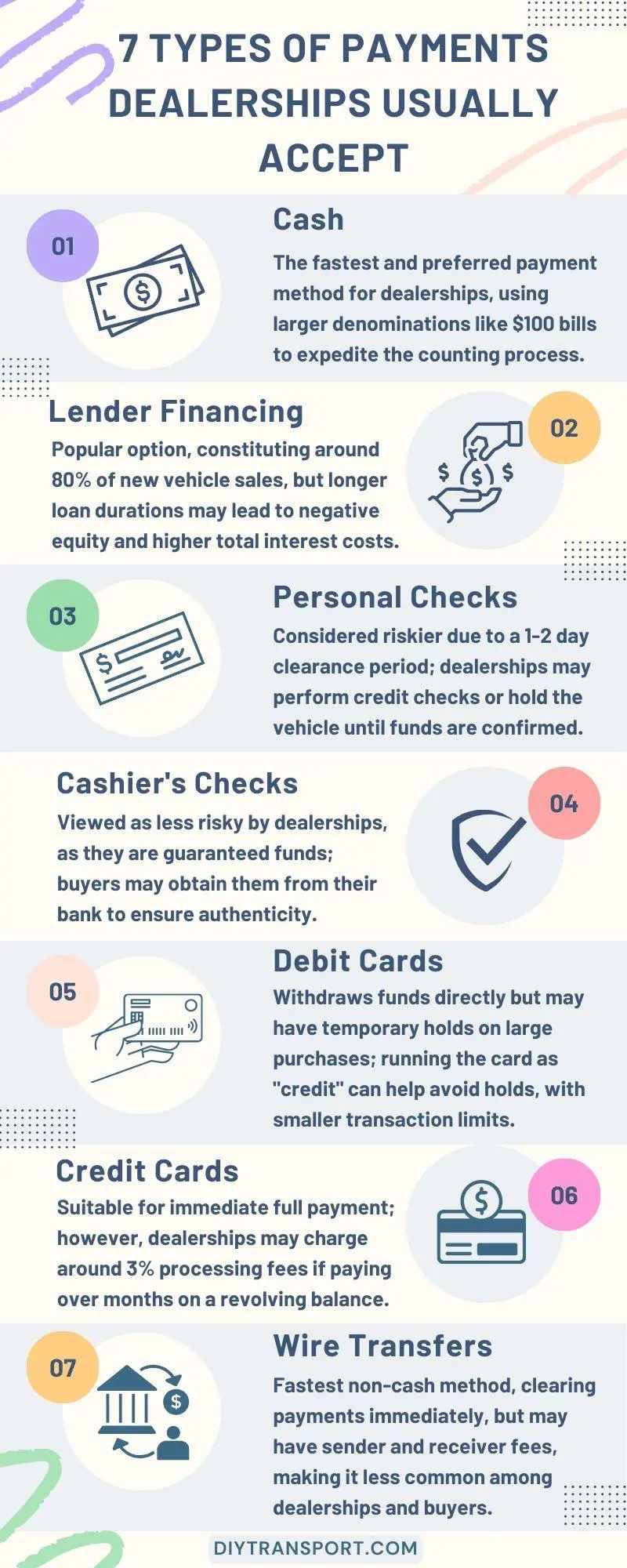

Types of Payments Dealerships Usually Accept:

Dealerships accept several payment options when purchasing a vehicle.

Cash

The simplest way to pay without financing is physical cash in the form of bills. Most dealerships prefer it due to being the fastest clearing payment method.

However, buyers should bring larger denominations like $100 bills to make the counting process less cumbersome for dealership staff.

Lender Financing

Financing through a lending institution like a bank or credit union is one of the most popular payment methods, accounting for around 80% of new vehicle sales. Terms are typically between 24 to 72 months.

Though longer loan durations may seem enticing with lower monthly payments, it increases the risk of owing more than the vehicle’s worth due to depreciation (negative equity). It also results in higher total interest costs over the loan’s lifetime.

Personal Checks

Some dealerships may accept personal checks from buyers, but it is considered one of the riskier payment options.

This is because the check can take 1-2 business days to clear the bank fully. As a precaution, dealerships may require a basic credit check or hold the vehicle until the funds are confirmed. The table outlines some standard practices dealerships follow regarding personal checks.

| Dealership Policy | Details |

|---|---|

| Acceptance with credit check | Dealers check the buyer’s credit history and bank balances before accepting the check. |

| Acceptance with vehicle hold | The buyer gets the vehicle only after the check fully clears, usually within 3 business days. |

| Denial of personal checks | Very few high-volume dealers may not accept checks at all to avoid any risk of bounced payments. |

Cashier’s Checks

Cashier’s checks, also known as bank checks, are viewed as less risky than personal checks by dealerships since they are guaranteed funds backed by the issuing bank. This allows buyers to finalize the sale quickly without worries of delayed clearances. Some buyers prefer getting a cashier’s check prepared at their bank to ensure the dealership it is authentic and can’t bounce like a personal check.

Debit Cards

Swiping a debit card withdraws funds directly from the buyer’s linked checking account. However, some banks place temporary holds of up to three business days on large debit purchases for verification. Buyers can request to run the card as “credit” instead to avoid this, but may still incur smaller transaction limits, typically under $500, depending on their bank.

Credit Cards

Using a credit card works for buyers who can immediately pay off the full balance. Otherwise, dealerships may typically charge processing fees of around 3% of the full purchase price if paying over months on a revolving balance. This extra fee still makes credit cards a less economical payment option for most vehicle buys.

Wire Transfers

An electronic funds transfer between bank accounts via account and routing numbers. It is the fastest non-cash method that clears payments immediately. However, it also usually has sender and receiver fees attached, making it a less common choice among dealerships and buyers.

Difference Between Personal, Certified, Cashiers Check

| Feature | Personal Check | Certified Check | Cashier’s Check |

|---|---|---|---|

| Issued by | Individual account holders | Bank directly from the holder’s personal account | Purchased directly from a bank |

| Verification of Funds | Relies on the account balance at the time of deposit | The bank verifies and certifies available funds | The bank is directly liable for the entire check amount |

| Bouncing Risk | Can bounce if insufficient funds at deposit time | Cannot bounce as funds are withdrawn at certification | It cannot bounce, as the bank is directly liable |

| Clearance Time | Takes time for funds to clear through the system | Takes a few days for the certified funds to clear | Funds are available immediately, with no waiting period |

| Required Signatures | Only the signature of the account holder | Both the bank’s and account holder’s signatures | Only the bank’s signature is required |

| Forgery Susceptibility | More susceptible to forgery due to fewer security validations | More secure against forgery with dual signatures | Highly secure, as it involves the bank’s liability |

| Cost | Usually obtained without fees | Banks charge a small certification fee (around $15-20) | Banks charge a higher purchase fee (around $10-15) |

| Cancellation | Can be canceled or stopped after issuance | Cannot be canceled after certification | Cannot be canceled once issued from the bank |

| Common Use Cases | Everyday transactions, but higher risk of non-payment | Higher security transactions with a few days wait | High-security transactions where immediate funds are crucial |

Let’s see these different types of checks in detail below:

Personal Check

A personal check is issued by individual account holders from their personal checking accounts. Funds from a personal check must clear through the banking system before the deposited check amount is made available in the recipient’s account.

Personal checks can bounce if insufficient funds are in the account at the time of deposit because the funds have not yet cleared. Only the signature of the account holder is required on a personal check.

Personal checks are very easy to obtain since banks don’t charge fees for issuing them. However, personal checks are more susceptible to forgery than certified or cashier’s checks due to the lack of additional security validations before deposit.

Certified Check

This one is issued by a bank directly from the holder’s personal checking account. With a certified check, the bank verifies that there are enough funds in the account to cover the check amount and stamps the check with a “certified” marker. This means that the funds are withdrawn from the account at the time of certification, so a certified check acts like cash and cannot bounce like a personal check.

However, it still takes a few days, like a personal check, for the funds to fully clear through the banking system. Both the bank’s and the account holder’s signatures are on a certified check, providing more security against forgery than a personal check. Banks typically charge a small fee, often around $15-20, for the service of check certification.

A certified check is more secure than a personal one but not as convenient as a cashier’s one since the funds take a few days to clear.

Cashier’s Check

A cashier’s check is purchased directly from a bank using cash, a cash equivalent such as a money order, or by authorizing a withdrawal from one’s personal bank account. The notable distinction is that with a cashier’s check, the bank becomes directly liable for the funds rather than verifying that the account holder’s funds are available.

Because of this, cashier’s checks are as good as cash and cannot bounce like a personal check can if stolen or lost. Cashier’s checks cannot be canceled once issued from the bank. The funds from a cashier’s check are available for use immediately without any waiting period for clearing, like with a personal or certified check.

Only the bank’s signature is required on a cashier’s check since no individual account holder is involved. Banks typically charge a higher purchase fee than certification fees for a cashier’s check, often $10-15, because it provides the highest level of security and certainty of funds of the three check types.

Cashier’s checks are commonly used when the risks of potential non-payment associated with personal and certified checks are unacceptable, such as when car dealerships accept personal checks. Due to the security and immediacy of funds, cashier’s checks offer reassurance to recipients in higher-risk transactions.

Key Takeaways

- Personal checks have the lowest security but are free to issue, and it takes a few days for funds to clear.

- Certified checks provide added validation through bank certification and signature but still take a few days to clear and cost a fee.

- Cashier’s checks are purchased with immediately available funds, require only a bank signature, but have the highest associated fees.

The level of security verification and immediacy of funds increases from personal to certified to cashier’s checks, but so do the monetary costs and effort required. For important or high-cost purchases, a cashier’s check may provide the highest reassurance accepted if the seller has questions about whether car dealerships accept personal checks due to the risks.

However, a certified check could work as a cheaper alternative that still significantly reduces the risks over a simple personal check, depending on the policy of the individual dealership. Buyers and sellers need to understand these check differences when negotiating terms of payment.

What About Delivery of the Car From the Dealer? Does The Shipper Accept Checks?

No, car shippers do not accept checks. You can make payments via cash (most preferred) and online payment wallets like Venmo, credit cards, and debit cards.

At Easy Auto Ship, we even give you a handsome discount of up to $150 on cash payments, depending on your total size.